Not too long ago, a CEPA emailed me and asked, “what is the cost of not having an exit plan or master plan?” I thought that was a great “ask” because I have never seen that question quantified. I wrote and told him I needed to think over that question. This is an attempt to provide that CEPA with some kind of intelligent answer.

My immediate response to the cost question is a common answer in the business of Master Planning, “it depends”.

Yes, it depends on a lot of factors: in fact too many to mention in this space. The real answer is that not having a plan can only be measured by three costs: loss of enterprise value, the morality cost of not doing the right thing, and the cost of timing.

The real cost of not having a plan is the cost of increased risks in each of the above areas!! Having a Master Plan greatly decreases your risk factors!!

Loss of Enterprise Value:

The biggest risk in all of these areas is the fact that business owners are human!!

What will be the effect if the owner is not involved or gone from operations forever??

I have seen statistics from the financial planning industry that says 50% of businesses who lose their owners because of disability or death become insolvent in two years.

There is no available guarantee that provides for owners to be around today, tomorrow, next month, next year, etc.

Just how is this risk quantifiable? Again, “it depends”! The size of the business, current business value, business operations assessment, industry, company resources, people, products, facilities, etc. all come into play in calculating the risk of being “human”.

If a Master Plan is in effect to “maximize the value of the business” as described in “Leg One” of a Master Plan and something happens to the owner, at least the blueprint for success and increasing company value is in place for others to implement.

THE MORALITY COST OF NOT DOING THE RIGHT THING:

Often a business owner is involved in being a “lifestyle” owner and they forget the “responsibilities” they have as a business owner. One the biggest they have is to their employees.

The company’s future success has a resonating effect on the success of each employee’s life and family.

BUT, if the owner doesn’t have a Master Plan in place and the business fails or their growth deteriorates and value decreases what is the cost effect of upon their employees and families????

How is that measured???

THE COST OF TIMING:

This cost covers a lot of risks in all legs of the stool.

In “Leg One”, what if products, services aren’t timed perfectly as they would be in a good Master Plan. How about the recruitment of personnel in a timely manner?

In “Leg Two” what about the timing of someone selling their business without appropriate financial planning? What if their financial resources fall short of the owner’s life span, etc.? What if there is no estate planning or poor planning and the business has to be sold to cover taxes when the owner dies?

How can the costs of these results be measured??

In “Leg Three”, what if they transition from the business without a life plan? What if family members aren’t involved? What if the owner loses their personal identification? What is cost of all of this personal non-planning?

SUMMARY:

I could write a book (and have) about this subject of “What is the Cost of Not Having a Master Plan or Exit Plan”.

Cost can only be measured in the “risks” that aren’t covered or are created without a plan in place.

Of course, the biggest risk that every owner must cover is the risk of being “human”!!!

This makes having a plan in place…………………………..mandatory!!!!

For more information, Contact Megabite Restaurant Brokers, LLC

Phone: (817) 467-2161 www.megabite-rb.com

How can Megabite Restaurant Brokers sell your restaurant, bar or nightclub business? You can discreetly and confidentially contact a broker at Contact Us, read other testimonials at Client Testimonials, search buyers at SEARCH OUR BUYERS or research more info here if you just want to understand how to SELL A BUSINESS.

Media Release from BizBuySell … 2016 Buyer-Seller Confidence Index: Small Business Sellers Remain Confident in Current Market but the Gap is Closing as Buyers Seeing More Realistic Asking Prices

BizBuySell

September 27, 2016

Both Buyers & Sellers Say Election Result Could Change Their Plans in the Market, Data Shows a Clinton Win Could Lead to More Sellers in 2017

San Francisco, CA – BizBuySell.com, the Internet’s largest business-for-sale marketplace, announced today the release of its 2016 Buyer-Seller Confidence Index, a national indicator of small business buyer and seller sentiment of the current business-for-sale environment. The confidence index is calculated by evaluating survey responses of more than 2,000 people interested in either buying or selling a small business. A separate score is calculated for both current small business owners interested in selling and prospective buyers currently exploring the market. Each group’s score ranges from 0 to 100, with 100 representing a perfect environment for buying or selling a business and a score of 50 representing neutral confidence.

This year’s survey results show that while sellers continue to feel more confident than prospective buyers in the today’s market, the gap is closing. The 2016 Seller Index stands at 59, down slightly from 62 in 2015, while the 2016 Buyer Index grew to 49, up from 47 a year ago.

Overall, the Seller Index did drop three points from last year, but the 59 score remain higher than the 56 reported in both 2013 and 2014. In fact, nearly 60 percent of respondents said they are confident that they would receive a price that met expectations if they sold their business today. A majority (65 percent) also believe that they could get either the same or a higher price than they could last year.

Looking at the Seller Index’s slight dip more closely, owners appear to be a little less confident in the future than they were last year. In 2015, 59 percent of sellers believed they could wait a year and receive a higher price for their business. In 2016, that number dropped to 48 percent. Concerns of those with lower confidence include fear of a depressed small business environment and economy (38 percent), increasing costs (31 percent), declining sales and revenue (22 percent), changing wage regulations (17 percent) and changing healthcare regulations (15 percent).

Similarly, this year’s survey shows that almost 48 percent of owners believe selling right now would be difficult in terms of time, effort and expense. Just 40 percent believed the same in 2015. So what is making it more difficult? The top reason why owners said they couldn’t sell right now was that they didn’t believe they could get enough money to fund their future plans, whether that be retirement, a new venture or another purchase. Others said they couldn’t find a buyer right now or didn’t believe their business was performing well enough.

“While the Seller Index fell a few points, overall optimism remains,” Bob House, President of BizBuySell.com, said. “We’re seeing rising financials from most of the businesses sold on our marketplace this year so it makes sense that now would be viewed as a good time to sell.”

Prospective Buyers Noticing More Acceptable Asking Prices, Improving Small Business Economy

As is evident by the increasing Buyer Confidence Index score, buyers appear to be growing more confident they can hold their own at the negotiating table. Seventy-three percent of buyers said they would be able to buy a business today for an acceptable price, a slight increase from the 70 percent that said the same last year. When asked what makes small business sale prices more acceptable this year, most potential buyers credit owners for setting a more realistic price (38 percent) while others attribute the change to an improving small business environment and economy (35 percent), less demand/competition for listings (29 percent) and increased supply of businesses for sale (23 percent). Interestingly, sellers list the small business economy as a concern but buyers are seeing it as a positive.

In the bigger picture, however, buyers remain less confident in the market than sellers. Naturally, buyers are suspect of the other side as 60 percent believe small businesses for sale are currently overvalued, compared with just 4 percent who believe they are undervalued. Because of this, nearly half of buyers said buying a business right now would be difficult in terms of time, effort and expense. Many didn’t see the environment changing either as only 29 percent said they thought they can get a better deal if they wait a year to purchase. Most (56 percent) said prices would likely stay at their current values in 2017.

For those buyers who are still waiting to pull the trigger, the key constraint appears to be limited supply of suitable businesses as opposed to availability of financing. This year’s top inhibitor to ownership was simply not finding the right business (44 percent), much more common than those who said they don’t have available capital (25 percent) or can’t find funding sources (7 percent).

“It’s good to see the gap closing between buyers and sellers and a more balanced market forming,” House said. “As we move closer to 2017, it will be interesting to see how variables like the election results impact confidence.”

Buyers & Sellers Say the Election Result Could Determine Their Plans to Enter or Exit Small Business Ownership

With the U.S. Presidential election fast approaching, it’s possible these confidence numbers could be influenced by the winner. It appears both buyers and sellers would be more confident under a Donald Trump presidency. Fifty-seven percent of sellers and 54 percent of buyers said Donald Trump is the candidate who would most improve the small business environment. Comparatively, just 27 percent of sellers and 31 percent of buyers feel Hillary Clinton would most improve the small business environment. Further, 53 percent of sellers and 47 percent of buyers believe the small business environment would worsen if Hillary Clinton was elected.

Perhaps more telling than voting direction is that a significant number of buyers and sellers say they will actually change their ownership plans based on who wins, specifically if the less-favored Hilary Clinton takes office. In fact, one in five sellers said they would be more likely to sell their business if Hillary Clinton is elected President. Similarly, 31 percent of buyers said they would be less likely to enter small business ownership if Clinton wins.

Clinton supporters said they might take similar action should Donald Trump win. Sixteen percent of current owners said they would be more likely to sell and 15 percent of buyers said they would be less likely to buy if Trump wins the election.

So just why is the election result so important to small business owners and prospective buyers this year? When asked what issues were most important to them, both parties list tax reform, health care, economic policies, and jobs in that order.

Sellers Not Fond of New Overtime Regulation While Buyers Actually Support Them

Beyond the election, another issue impacting the small business community is the new Department of Labor overtime rules. Effective December 1, 2016, the new rules mandate any employees making less than $47,476 annually must be paid at least time and a half their regular rate of pay for any hours worked in excess of 40 a week.

Not surprisingly, small business sellers (the owners soon to be directly affected), were more likely to be against the changes. More than a third (37 percent) were against the changes, while 29 percent were in favor of the regulation changes; 22 percent have no opinion and 11 percent said they were not aware of the changes. Looking at the future, almost half (48 percent) of soon-to-be sellers believe the new overtime regulations will decrease the value of small businesses.

Buyers, on the other hand, were more likely to agree with the purpose of the overtime changes. In fact, most (41 percent) prospective buyers are in favor of the overtime changes, and the majority (80 percent) said the changing rules will have no effect on their plans to purchase a small business. It’s possible these buyers see a bargaining chip for the future purchase. Forty-eight percent said the overtime changes will decrease the value of small businesses.

About the BizBuySell’s Business Buyers-Seller Confidence Index

BizBuySell.com is the Internet’s largest marketplace for buying or selling a small business, with over 1.6 million monthly visits. The company releases its Business Buyer-Seller Confidence Index on an annual basis, reporting changes in buyer and seller opinions of the current business-for-sale environment. The index and scores are calculated through a number of weighted survey questions issued to over 2,000 people currently interested in either buying or selling a small business. For more information on the survey findings and index scores, please contact BizBuySell directly.

Media Contact:

Bobby Chilver

Walker Sands Communications

office: (312) 546-4712

How can Megabite Restaurant Brokers sell your restaurant, bar or nightclub business? You can discreetly and confidentially contact a broker at Contact Us, read other testimonials at Client Testimonials, search buyers at SEARCH OUR BUYERS or research more info here if you just want to understand how to SELL A BUSINESS.

I cannot recommend Jeff Adam highly enough. He maintains a grasp of all of his transactions and never seems to be at a loss of what is going on in each. I have on numerous occasions discussed with Jeff’s clients their appreciation of the personal service he provides whether the transaction involves $100,000 or is a multimillion dollar transaction. If you are looking for someone who understands each and every facet of your business or transaction, you will not be disappointed in choosing Jeff Adam.

Franklin Cram, PC, Attorney at Law

For more information, Contact Megabite Restaurant Brokers, LLC

Phone: (817) 467-2161 www.megabite-rb.com

Megabite Restaurant Brokers can help you value, sell or buy a restaurant, bar or nightclub business. You can discreetly and confidentially contact a broker at Contact Us, read other testimonials at Client Testimonials, search buyers at SEARCH OUR BUYERS or research more info here if you just want to understand how to SELL A BUSINESS.

At least once a week, we find ourselves looking through adjustments made to earnings before interest, taxes, depreciation and amortization (EBITDA) on a business for sale, and saying, “What in the world…?”

Adjustments can be perfectly acceptable. Owners run excess personal expenses through their business that would not be assumed by a future owner (i.e., fun trips, memberships). Sometimes, family members are paid far-above-average salaries and will not be continuing with the company. On justifiable adjustments, you’ll hear no contest from us. However, just because adjustments are justified, doesn’t mean they’ll leave a good impression on investors. We recently saw a business barely breaking even with a sizable adjustment for private air travel; such adjustments speak volumes about priorities.

Lately, we’ve started tracking some of the bogus adjustments people try to deduct out of companies. Here are some anecdotes illustrating how wishful thinking intersects with the bottom line.

Owner Compensation

The most common add-back is completely subtracting owner compensation, boosting the supposed bottom line by between $200,000 and more than $1 million. Yet, they are usually the leader(s) of the company.

Some owners work full-time, while others are serving in more of an advisory capacity, but unless they permanently reside in another state without any oversight of or contact with the business (including financial), they are doing something worth a dollar amount. That figure may not be the same amount they’ve been paying themselves, but it’s definitely not $0.

Leadership Compensation

A 150-person company had a leadership team of five people. All the leaders were paid quite well, based on below-market salaries and generous performance-based incentive compensation. The CIM argued that they were paid too well for the industry. So, each person’s salary was adjusted down to an industry average, reducing the overall leadership compensation pool by more than $600,000. When we inquired as to whether the current team would be staying post-transaction and under what conditions, the intermediary explained that the adjusted salaries were meant as a starting point and that each leader expected to renegotiate his/her total compensation with the new owner, including base salary, incentives, and equity.

Imagine walking into a company and saying to one of the key leaders, “Hi, we’re your new owners. We’ve heard you’re an essential leader within this company we need to work hard to keep, but we’re going to reduce your salary down to the industry average.” Would you stay? Why should a buyer account for less than anticipated compensation?

Sub-Contracted Labor Costs

A manufacturing company kept a lean full-time team, and used sub-contracted labor during seasonal periods, which is perfectly reasonable. What was not reasonable was the more than $200,000 adjustment for “excess costs of sub-contracting.”

A company can’t have it both ways. A bigger team means bigger year-round operational costs. A lean team means you take a hit when extra labor is required. Pick the operating style and own it.

Marketing Expenses

A particularly courageous CIM presented a list of adjustments that included more than $200,000 in marketing expenses. We immediately requested further explanation and were told that it was an ineffective online marketing campaign the company had run the previous year for a new product line introduction.

Ineffective spending is still real spending. Enough said.

“One-Time” Expenses

Adjustments related to one-time expenses are quite common. Two examples of creative implementation include the cost to develop a company’s website and inventory write-offs conducted every year.

There are occasional one-time expenses that should be adjusted out, but they are rare. We often find lots of recurring non-recurring expenses. More often, these expenses represent necessary costs of doing business above and beyond the line items that normally appear on a company’s annual income statement. The bottom line is that, regardless of whether it’s normal, if it’s a necessary cost of doing business, it shouldn’t be adjusted out.

Research & Development Expenses

Companies seeking to grow must engage in ongoing investment, including R&D. In one recent case, the revenue from a new product line was included, but the associated costs of developing that line were adjusted out.

New revenue streams aren’t delivered by stork. Sustainable businesses require ongoing investment, which a buyer will have to invest in as well.

Retroactive Change Benefit

Two recent CIMs added back projected savings from recent, or even yet-to-be-fully-implemented, changes in process or software retroactively to previous years.

You can’t change the past. The best way to present effective change improvement is to provide evidence of its actual impact and how it might look in the future.

Legal Fees

A company had an unfortunate two-year legal battle. The CIM adjusted out over $700,000 in legal fees related to the “one-time litigation event.”

If a company must enforce its position by legal action, or if its customers, suppliers, or competitors initiate suits against it, the company must spend real money. That won’t change with ownership, and evidence of a substantial legal history will tell a prospective buyer that such events must be accounted for in projections and valuation.

A productive question to ask in making EBITDA adjustments is whether a public company could deduct such expenses to boost earnings presented to shareholders. Can a CEO be adjusted out? Can a leadership team’s salaries be calculated as industry averages rather than what a company actually pays them? Can a website exist, be regularly updated, but not actually cost anything? No, unless you’re Enron.

Including EBITDA adjustments from Crazytown may help you feel like you’re presenting a better illustration of the company’s earnings potential for a prospective buyer, but it’s counterproductive. These types of adjustments create distrust with prospective buyers. And buyers are generous in estimates they must make independently. If you leave a gap, such as assuming there will be no acquisition costs in hiring competent leadership, the buyers will inevitably insert a big round figure into their formula to cover all unknowns.

The best advice on creating a list of adjustments? Be honest and conservative. The relationship with buyers will start out on a much warmer and productive path.

ABOUT THE AUTHOR

NAME: Brent Beshore

Brent Beshore is the founder/CEO of adventur.es, a family of companies investing in family-owned companies throughout North America

Often when you decide to sell your business, you’ll find that many aspects of the business are not ready for a sale. Whether it’s incomplete financial statements, disorganized tax history, or simply miscommunication, the sale process can quickly become complicated and difficult. While it’s possible to prepare your business for sale rather quickly, these band-aid fixes will not be overlooked by diligent buyers.

The lack of planning unfortunately leads to lower sale prices and money being left on the table. Ryan Guthrie, Director of the Private Equity Practice, BDO USA, said, “The majority of business owners who sell their business don’t plan ahead in preparation of a sale. In most cases, a lot of things that could have increased the value of the business and decreased the risk for buyers were not done.”

So what can be done to prepare for an exit with an uncertain time horizon?

1) EXECUTIVE MANAGEMENT

The most essential step that a founder can take to prepare the business for sale is to build out a full management team that can run the business without you. While it takes significant time and attention to prepare a competent management team, it’s one of the most necessary ingredients for a profitable exit. With a strong management team, interested buyers can feel confident that the business will be prepared for most transitions, including the departure of a CEO. If a buyer doubts the ability of the company to run in the absence of the founder, it can prove an insurmountable deterrent.

These concerns are not limited to owners near retirement age either. Young owners have little incentive to remain involved once the business has been sold. Scott Humphrey, Executive Managing Director and Head of U.S. Mergers & Acquisitions of BMO Capital Markets, said, “In the case of an exiting owner, the buyer needs to come in and not only get comfortable with the business, but ensure the business will continue to grow without the owner. This increases risk greatly.”

2) MIDDLE MANAGEMENT

Larger middle-market companies often prepare for a sale by bolstering management, but far fewer companies take the initiative to develop a strong set of middle management talent. Expanding the management capabilities beyond the executive level reassures buyers and ensures a seamless post-sale transition. Many buyers of businesses are looking for well-run companies that have fairly independent and strong business units that will transition nicely after the sale.

3) FINANCIALS

While a common best practice is to prepare an audited set of financial statements two years before a sale, there are also financial preparations that can take place much earlier that will help ready a business for an exit. Foremost among them is the process of separating out the company’s real estate holdings from the rest of the business. Robert Snape, managing director at BDO Capital Advisors, said “we’ve often seen owners carve out the real estate from the business and sell the business to one party and sell the real estate to a separate buyer.” However, if an exit is a possibility in the next five years, Guthrie at BDO advises against making dramatic changes like relocating a factory or any other business change that would appear to disrupt a growth trend. If the real estate is held separately from the business, often you can sell the business and then lease the factory or warehouse back to the business owner to retain some of the earnings even after you exit the company.

4) CUSTOMERS

When there is a long-term horizon of sale, it is also beneficial to look at ways to add to the sustainability of earnings. Buyers want to see customer diversification and reduce the risk of losing key customers that would depart with the founder, especially if those customers make up a significant portion of the revenue. Data from Axial shows that the average amount of interest in purchasing a business is lower whenever there is significant concentration in a few larger accounts.

5) CORPORATE STRUCTURE

It is important to examine the corporate structure of the company. There are important tax consequences that come with selling C-Corp and S-Corp businesses. Guthrie advises company owners to keep the end in mind and to determine what the optimal corporate form would be for the business. “There’s not a lot you can do a year before the sale,” he warns. “But there’s a whole lot more you can do 10 years before the sale.” Checking with your accountant to ensure everything is set up correctly for a potential sale can have an effect on the final valuation of your business.

It is more crucial than ever for owners to plan ahead to maximize the enterprise value of their company. If the past several years have provided any lesson to sellers, it is that company valuations are at the mercy of the marketplace and business owners will want to be ready to take advantage of market timing.

Selling a company is a long and complex process. Preparing for a sales process takes at least 12 months, and then the actual process itself can take another 12 months. If you think of selling your business as something similar to a very long multi-year enterprise sales cycle, you’ll begin to realize that a business sales process is like any other sale process in that it can be broken down into its core component stages and elements.

This article provides an overview of the key stages of an M&A sale process, whether it’s for a lower middle market company, a large public company, or anything in between.

STAGE 1: DEFINING POTENTIAL OPTIONS AND EXIT STRATEGIES

When considering the sale of a business, there are potentially a wide variety of transaction options. These options must be understood and evaluated by the CEO, owner, and/or board. Understanding these options and the decisions they lead are the most strategic decisions a company will ever make when it comes to realizing value. Leveraged buyout, strategic M&A sale, minority recapitalization, ESOP, etc — these are all fancy investment banker terms but they essentially boil down to various methods by which a company sells itself or part of itself or to whom it sells. Buyers break down at a high level into two categories: financial buyers and strategic buyers. They both have their pros and cons. Neither one is better by nature, it’s highly situational. A good M&A banker will work with the business owner to understand the selling requirements, the range of valuation expectations, and strategic goals. This also includes defining: exit strategy alternatives; thinking through the most appropriate types of acquirers; timing of sale; tax consequences and owner’s desire for future involvement with the company (or lack thereof).

STAGE 2: DETERMINING A VALUATION RANGE FOR THE COMPANY

Determining a reasonable valuation range is a critical step in the process. If the banker thinks they can achieve a valuation range that isn’t acceptable to the owner, the process should stop right there. Too many deals get derailed by sellers and buyers having completely different expectations about business value. While it’s the job of the banker to close that gap with negotiation prowess and transactional expertise, immense gaps can’t be bridged no matter how skilled you are. Valuation technique ranges from the highly academic and analytical methods of discounted cash flow and dividend discount models (DCF and DDM) to the more pragmatic comparable company valuation methodologies. Unfortunately, none of them is a replacement for the actual process of engaging with high quality and highly relevant buyers. Analysis and number-crunching is necessary but not sufficient, and will only take you so far. In the end, the price is determined in the market by the buyers and the quality of your engagement with them.

STAGE 3: PRE-MARKETING VALUE ENHANCEMENT

Often, Advisory firms will review a company’s strategic and financial condition and have suggestions for how the company, over a 6-12 month period, can make some changes to make it more desirable. These should not be massive changes in strategy because those take too long and are risky, but should be valuable changes to management team or business strategy that make the business more attractive in a reasonably short period. Sometimes a trigger-happy CEO just wants to sell the company, but the best thing to do is make some changes and adjustments first before going to market. Again, working with a knowledgeable banker or informed board members that have relevant industry experience and business strategy context can be very valuable.

STAGE 4: INFORMATION GATHERING, DATA COLLECTION, AND PRESENTATION

Spending the time to properly aggregate, interpret, and present a company’s financial and business history and future projections is a crucial element of the sale process. This requires trust between a business owner and his M&A Advisor because at this point, the kimono is being opened. The engagement letter should reflect the confidentiality that an investment bank commits to before they have access to such sensitive information. Business owners typically prepare their financial statements for tax purposes, not for business sale purposes. Using tax statements for business sale presentation is a major mistake, as it usually obscures the earnings capability of a business. Taking the time properly present a company’s earnings power can have a big impact on how the buyers view the opportunity. Of course, the seller can go too far here and lose credibility, which is also a big mistake in the other direction. However, making sure that the appropriate financial adjustments are made is an important step and takes time and analysis by the CPA and the M&A team.

STAGE 5: MARKETING MATERIALS PREPARATION

When potential acquirers evaluate a company, they expect the records and facts to be properly organized and documented. Disorganized or poorly collated material on a business delays the process, looks sloppy, and therefore hurts the seller tremendously. It’s another area where many sellers are pennywise and pound-foolish and pay a terrible price for trying to save money in the wrong place. Well-packaged and presented business summaries increase a buyer’s confidence and comfort level and increase the likelihood of a successful sale. A business owner spends years establishing name recognition, market niche, vendor relationships, operation & production systems, management, personnel, distribution channels, customer loyalty and numerous other intangibles. This is a story that needs to be properly told to educate potential buyers.

STAGE 6: BUYER RESEARCH AND BUYER OUTREACH STRATEGY

While large multi-billion dollar companies often have only a handful of relevant and sufficiently capitalized potential acquirers, lower middle market companies (this generally refers to businesses whose value ranges generally between $10M and $250M) often have an enormous number of potential buyers. Some of these potential buyers are known to the business owner, some might be known by the Advisor, but no one’s rolodex is usually broad enough to know every potential buyer. This means that the banker and the business owner must have tools and resources to research and access the largest and most qualified data set of relevant buyers. Databases and tools of varying qualities exist out there, but there is no silver bullet. This research process should be exhaustive, not rushed. The banker should review competitors, customers, strategic buyers, private equity firms with relevant expertise, and other sources of highly suitable capital and partnership. This is one of the most time-intensive elements of the process but it often determines the overall success of the sale process. If you don’t approach the best buyers, how can you get the best outcome?

STAGE 7: QUALIFICATION OF POTENTIAL BUYERS

Many potential buyers that express interest in a business will not be qualified to purchase the company. These companies are referred to as tire-kickers. A good banker will know the right questions and have enough market intelligence and expertise to smoke these buyers out and pre-qualify the right potential acquirers before the tire-kickers impact the CEO or management team’s time and attention. This isn’t a particularly complex or time-intensive step, but if it isn’t done, the CEO will waste a lot of time and effort speaking with unqualified buyers and increasing the confidentiality risk of the entire process.

STAGE 8: NEGOTIATION PROCESS

There are many schools of thought on how to run the negotiation and buyer engagement process. Some Advisory firms suggest a negotiated process with only one highly targeted buyer. This strategy has tremendously high risk but can be extremely expedient if it works out. In general, Sellers are more likely to achieve a stronger outcome when negotiating with multiple qualified buyers, rather than just one or a handful. This can of course be taken too far as well, where every buyer feels like they are part of a huge auction process, in which case they walk away for fear of over-paying. Competition in a sale process does typically drive up purchase price and quicken the pace and accountability of buyers, but it should be handled carefully, respectfully and professionally.

STAGE 9: TRANSACTION STRUCTURE

The sale of a business has many financial and professional considerations for the management team / owner. The purchase price is only one component of the overall result. Other decisions and considerations include: stock sale versus asset sale; earnout; terms and interest rate on financing; liabilities assumed by the acquirer; employment contracts; non-compete agreements; current assets retained by the seller; stock ownership and equity options packages; relocation; employee preservation versus redundancy layoffs, etc.

STAGE 10: IOIS, LOIS, AND PURCHASE AGREEMENTS AND CLOSING

Typically, buyers express interest in a company at three stages through three documents: the IOI, LOI and Purchase Agreement. The IOI is non-binding and provides the proposed terms, valuation and structure for a transaction. The owner will review this with their banker and make a determination as to whether or not to invite the buyer to learn more about the company and become more serious. LOIs (letters of intent) are a more serious signal of interest by the buyer; once they are jointly executed, the seller is typically under exclusivity with that buyer, such that they are not able to meet with other buyers during a stated period of time. Meanwhile, that buyer is beginning to conduct heavy due diligence on the business with the intent of acquiring it. During the exclusivity period, the buyer must move quickly to determine if they want to proceed. If so, the purchase agreement must be drafted to define all the details of the transaction: legal, financial, representations, warranties, etc. The purchase agreement is the definitive document outlining the terms of the sale.

STAGE 11: POST-CLOSING ISSUES & BUSINESS TRANSITION

The transition period typically involves a period of cooperation during which time the seller will assist the acquirer in transition. There are instances in which the seller is specifically not interested in doing this, however a lack of willingness to ease the transition typically lead to a lower valuation and in plenty of cases can derail the deal process entirely. Sellers should proceed with extreme caution if they elect to have no post-closing commitment. Post-closing commitments often include transferring customer relationships, explaining key management or market dynamics, and other proprietary information and trade secrets needed to operate the business optimally.

Solidify These 5 Business Fundamentals Before You Grow

By Shindy Chen | October 29, 2015

Every company’s primary purpose is sustained growth. This may involve seeking outside investment, raising capital, or joining and/or acquiring a like-minded company with a similar product, service, or market.

But putting the cart before the horse can do more harm than good to the business and most importantly, its customers. Before getting bigger, it’s essential to ensure the following key fundamentals are in place.

People

Anyone will tell you that having the “right people” is essential to growing a company, but what does this mean, exactly? Managers who were trained to carry out responsibilities based on existing arrangements, methods, and concepts may not be ready to adapt to new models, workflows, employees, or even leadership. “Understand that some managers cannot handle growth-oriented initiatives—make sure they’re in line with the goals being sought,” according to company growth strategist Marc de Swaan Arons in Forbes Magazine.

Targeted growth training prior to expansion may be necessary to ensure managers can continue to guide and empower others. Companies can start by tapping their HR teams to develop any additional outreach or training programs required, and to ensure leaders are informed and delivering consistent messages.

Culture

With each major addition in the workforce, a company’s intrinsic culture is at risk of dilution. That’s not necessarily a bad thing. Like living beings, company cultures are always evolving, and any change in regards to size or process will make an impact. To help the company evolve successfully, gather high level company officials to review mission statements, workflows, key tenets of the business, and achievements. Re-stating the core principals that have gotten you this far will help you continue to uphold them as the company moves forward.

Technology

What technology tools are employees using to communicate with each other and perform their day-to-day work? Can these tools support high demand, more complex processes or a larger organization?

Just because existing tools perform basic functions doesn’t mean that they’ll be the best tools going forward. Oftentimes, company employees and leaders will already have solid ideas about what potential tools, methods, and software might be better suited to get things done. Heed their suggestions. Before integrating or adopting to new technology, be sure to test it among small groups and roll it out in small batches.

Transparency

Employees and customers at every level share a certain level of anxiety when they learn that a company is expanding, merging with another, or being acquired. Don’t blindside employees — be sure to deliver timely internal messages regarding fundraising or a merger or acquisition.

For customers, it’s essential to detail the benefits of upcoming developments and , and whether anything, especially their experience, will change on their end.

Structure

Are the company’s departments set up for expansion? According to a McKinsey and Company report, “Well-defined organizational structures establish the roles and norms that enable large companies to get things done. Therefore, when growth plans call for doing things that are entirely new — say, expanding into new geographies or adding products — it’s well worth the leadership’s time to examine existing organizational structures to see if they’re flexible enough to support the new initiatives.”

A traditional retailer may choose to operate a new subset of outlet stores with management at arm’s length for maximize efficiency and autonomy. A product company that has typically used an executive panel to approve new products may find this model unscalable with an influx of new products and innovation. Thus it’s necessary to evaluate what processes can feasibly carry the business forward.

Company leaders are responsible for performing not only a thorough SWOT analysis but also evaluating the above qualitative components before getting bigger — or risk internal disorganization and pushback. Each company is different and has its unique growth drivers, but these solid principles will help address the basics.

ABOUT THE AUTHOR

NAME: Shindy Chen

Shindy Chen is the founder of Scribe, a content consultancy. She curates, writes, and edits for clients in the finance and tech industries. She also contributes to The Huffington Post and is author of The Credit Cleanup Book (Praeger). She was previously a Vice President in consumer lending at Wachovia Bank, and worked in financial broadcast media at CNBC and Bloomberg TV.

Five mistakes that could make it impossible for you to sell your business

BY: JACOLINE LOEWEN

Special to The Globe and Mail

Growing a business into a going concern can take years. Yet the strategies, relationships and the legal contracts that were critical to developing the business can turn into skeletons in the closet when it comes time to sell.The gap in differing views between buyers and sellers is interesting. Yes, there is the sale price and value an owner thinks the company is worth, and there is the final sale price. There are also features that sellers think are a priority during the sale process, but buyers don’t. Sellers think their product or services are the highlight of the business overview, for example, yet it is the legal areas that are often the first area to be explored by the buyer’s team at the start of the due diligence process.Each company is a unique situation. However, owners can gain a general understanding of the critical legal issues that will, at the least, lower the selling price or, worst of all, cripple and end the sale of a business:

1. Fuzzy ownership of intellectual properties can be a sinkhole. IP legal contracts apply to the work created by internal employees, but don’t forget to include the external and independent consultants’ work. Jim Balsillie spoke recently at the Empire Club in Toronto with Jacquie McNish and Sean Silcoff, two Globe and Mail journalists who wrote about the fall of BlackBerry (formally RIM) in Losing the Signal. Balsillie’s big takeaway is that the failure to secure intellectual property will be the critical downfall to a Canadian company’s value, and he shared how much it hurt Blackberry behind the scenes as well as publicly.

2. A lack of shareholder agreements with minority owners that permit majority shareholders to force a sale will be an issue. Often, the minority shareholders could prevent a sale and this will take up time and resources to resolve.

3. Share issuance to outsiders – such as former employees and advisers who are no longer on the scene and difficult to contact – will make the buyer concerned that they will not be able to buy the whole company. For startup technology firms in particular, it pays to have contracts to advisers and early employees done by lawyers who know the issues that can occur years into the future. Employees can be forced to sell shares upon leaving the company.

4. Former employees bearing a grudge may see the sale as the time to make their case public. Also, with online forums that encourage people to “Rate my Employer” former employees can make all sorts of claims. One company that placed advertising globally had just one bad comment on an online rating forum, questioning if the business was running a scam. This went unaddressed but was picked up during a simple Google search, raising just enough of a red flag and the buyer walked.

5. Real estate assets being mixed in with the holding company. When it comes time to sell the business, perhaps the real estate is not to be part of the sale. Instead, a common strategy is to keep ownership of the real estate. Sometimes the new owner might even lease the real estate, but a lack of separation of the real estate from the holding company will make this difficult to do.

Facing up to these five legal challenges will keep the buyer happy and interested in closing the deal. The seller will be confident that the ownership is clearly defined and the control of the company can be handed over to the buyers properly. Early identification of these issues will mitigate their impact and give the opportunity to improve the sale process. Long standing exit preparation such as these five legal points will make the owner look professional and the sale price not so high after all.

3 Ways to Enhance Your Credibility in the Business Selling Process

It takes a lot of time and effort to put together a deal to sell a middle market business. When these deals fail, it can be tremendously disruptive to your entire organization. Sometimes companies are on a specific timeline to sell and when a sale doesn’t go through it lowers the future price. That is why when you interact with a buyer, the goal is to ensure that you and your company are highly professional and credible. Here are three ways to enhance your credibility and avoid common mid-market deal killers.

1. Make Disclosures Upfront

When buyers are assessing a company, they are attempting to understand the ins and outs of the business as best as possible. As a result, buyers will want to see the strongest parts of the business as well as what is less than perfect. When sellers try to present too sunny of a picture, they can end up losing credibility. In fact, when a buyer sees a company that is presented with no negative issues it can be a red flag.

This is why any serious issues should be disclosed early in the process. Discovering major problems in due diligence can ruin a deal. Buyers end up feeling as though the seller is no longer believable if key information has been withheld. Plus, the due diligence process should be about confirming everything a buyer has been told, not evaluating whether the supplied information is valid or not. You can maximize your credibility and avoid these issues by making sure that any negative and potentially inflammatory issues are presented in the beginning; in this way, the buyer can properly evaluate these issues and even try to minimize their potential impact.

2. Maintain Consistent Messaging

If there are business strategies that will be communicated to buyers, it is important that all team members present a coherent picture. Make sure that everyone who will be communicating with potential buyers is on the same page. Consistent messaging is key.

3. Under Promise and Over Deliver

Another issue that can harm your credibility is falling short of forecast results. If you do not reach your year-end financial targets, this can scare a buyer. They expect predictability in revenues and earnings and will use that information to formulate their offer. That’s why it is essential to be cautious about presenting financial forecasts. Of course, buyers cannot expect you to be completely on target. It’s probably best to be conservative and leave a margin of error.

The best strategy is to over deliver and present numbers that are lower than what you realistically expect. This way, buyers are pleasantly surprised if your earnings are more than they expected. That’s far better than leaving them wondering why your forecasts were so high and your earnings so low.

If issues pop up that damage your credibility, it can be a red flag to buyers and damage a deal in progress. Follow these three strategies and you’ll be far more likely to keep buyers engaged and impressed.

AVOID 3 Mistakes that can Prevent You From Selling Your Restaurant by following this advice:

By: Mary Ellen Biery

Research Specialist, Sageworks

If you’re one of the millions of Baby Boomers and others thinking of selling your restaurant in the next several years, consider this: The top mistake sellers make is having unrealistic expectations, according to a recent survey of business brokers and advisors. Poor financial records and declining business sales are two more.

By many accounts, the number of businesses on the market is on the rise, with the retirement of Baby Boomers a main driver.

Indeed, 2 out of every 3 private-business owners surveyed recently by Pepperdine University said they expect to transfer their ownership interest within the next 10 years.

Unfortunately for many of them, a deal might never happen.

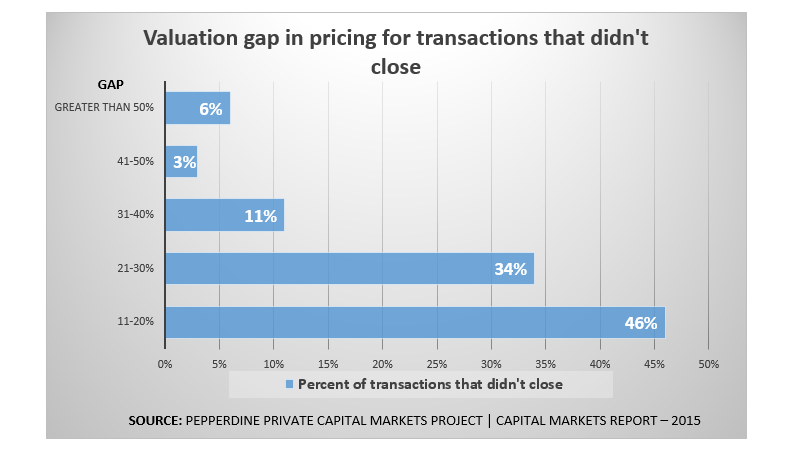

A separate Pepperdine-led survey of business brokers, found that more than half of their deals for Main Street businesses — those with revenues of $2 million or less — terminated without a closing. Rates for busted deals were especially high among the smallest firms, according to the survey by Pepperdine, The International Business Broker Association and M&A Source.

And while brokers and advisors weren’t asked to give the specific reason deals fell through, they and respondents in past surveys point to unrealistic asking prices.

“Business owners don’t know what they don’t know,” said M&A Advisor Scott Bushkie, principal of Cornerstone Business Services Inc. and a Certified Business Intermediary. “Most have only had one business in their lifetime, and it’s their nest egg. They hope and pray it’ll be as big as they need it to be to get them through retirement.”

Like a proud parent, these owners see the business in the most favorable light possible when it comes to pricing, Bushkie said. “When you come in overpriced, you might find buyers who are really intrigued about your company and who are great buyers, but they start thinking, ‘This person’s crazy’ or ‘No way can I get this financed,’ so it sits on the market too long.”

Bushkie recommends business owners plan in advance by periodically seeking valuations or even less formal estimates of value along with a market analysis.

Another top mistake that hurts sellers’ chances of a sale is when the business has poor financial records, according to the survey. “It all comes down to credibility,” Bushkie said.

The key, then, is an early start, according to Brian Hamilton, chairman of Sageworks, a financial information company.

Entrepreneurs are often good at the daily operation of a business — knowing how to make the product or generate sales. But because understanding financial statements isn’t as obvious to some of them, they may think of examining them only around tax time, Hamilton said.

“Smart business owners will use their financial information anytime they are making a decision about their business,” he said.

By using sound financial information, owners have a better opportunity to develop the long-term value of the business required by their personal and professional plans, according to Hamilton.

Even small businesses without the resources to hire top talent full time can get their books in order, and Bushkie recommends they do so at least three years prior to selling. Whether it’s a bookkeeper for five hours every two weeks or reviewed financial statements from an accounting firm, the efforts will boost business credibility when it comes time to sell, he said.

The final mistake that hurts sellers’ chances of a sale is declining business sales, according to the Pepperdine-led survey.

“Sales growth is an important metric because it shows the potential buyer how products and services are being received by the market,” Hamilton said. “In addition, since sales dollars are used to pay for expenses, which continually increase, it’s important to have healthy sales growth.”

Bushkie considers weakening sales growth more of a symptom than a reason deals go bad. “Unfortunately, most business owners make the decision to sell more of an emotional issue than a financial issue, and they end up holding on too long. When the passion’s gone and it’s not fun anymore and they’re not in it 100 percent, six to nine months later, the business starts showing the symptoms of them checking out,” he said.

One client had been profitable for 80 years but the year the owner decided to sell was the first unprofitable one. “Guess which year the buyer puts the most value on?” Bushkie said. “The client probably lost 30 to 40 percent value in their company just because they held on one or two years too long.”

Focusing on sales growth is especially critical in the years leading up to a possible sale. For many privately held companies, sales trends now are as good as they’ve been in years. The market for selling may also be peaking, Bushkie said.

“On the small Main Street deals, I would say that as far as the economy, stability in the marketplace, confidence in the marketplace, political issues going on or not, lending, interest rates — if it’s not a seller’s market right now it’s not going to be one for quite some time,” he said.

Follow Mary Ellen Biery on Twitter: www.twitter.com/MELloyd

Shared from http://www.huffingtonpost.com/mary-ellen-biery/3-mistakes-preventing-you_b_7291524.html

ABOUT THE AUTHOR

Mary Ellen Biery is a research specialist at Sageworks, a financial information company. She is a veteran financial reporter whose works have appeared in The Wall Street Journal and on Dow Jones Newswires, CNN.com, MarketWatch.com, CNBC.com, and other sites. She received her undergraduate degree from Wake Forest University, where she graduated cum laude, and her master’s degree from the University of North Carolina at Chapel Hill.

For more information, Contact Megabite Restaurant Brokers, LLC

For more information, Contact Megabite Restaurant Brokers, LLC